What is a Balanced Scorecard? Definition, overview, and examples

Companies need a well-defined strategy in order to be successful in the long term. After all, only with a broad goal and a roadmap for getting there is it possible to maintain an overview, prioritize issues and focus on the essentials. Over the years, a number of management methods have been developed to help with that – one of them is the Balanced Scorecard (BSC).

In this article, you will learn what exactly the Balanced Scorecard is, how to use the Balanced Scorecard in strategic management, and what parallels it has to Objectives and Key Results (OKR).

What to expect:

- What is the Balanced Scorecard? Definition and origin

- BSC in strategic management – how it works

- How good is the Balanced Scorecard? Advantages and disadvantages

- BSC and OKRs – a perfect combination?

- Conclusion: A stronger twin pack

- Balanced Scorecard – FAQ

What is the Balanced Scorecard? Definition and origin

The Balanced Scorecard (BSC) is a management tool from the 1990s that helps companies set strategic objectives and performance measures that are closely linked to their vision, mission and strategy. For this purpose, one creates an overview – the actual Balanced Scorecard – in which the most important goals of a company are presented and directly linked to key performance measures.

The Balanced Scorecard thus makes a company's strategic planning and key performance indicators visible in a simple way. The company's vision and mission become comprehensible to all employees – and it is possible to see at any time whether the strategic objectives have been achieved and whether the company is “on track”. Here, it is crucial that only the goals that are really important for the company are mapped.

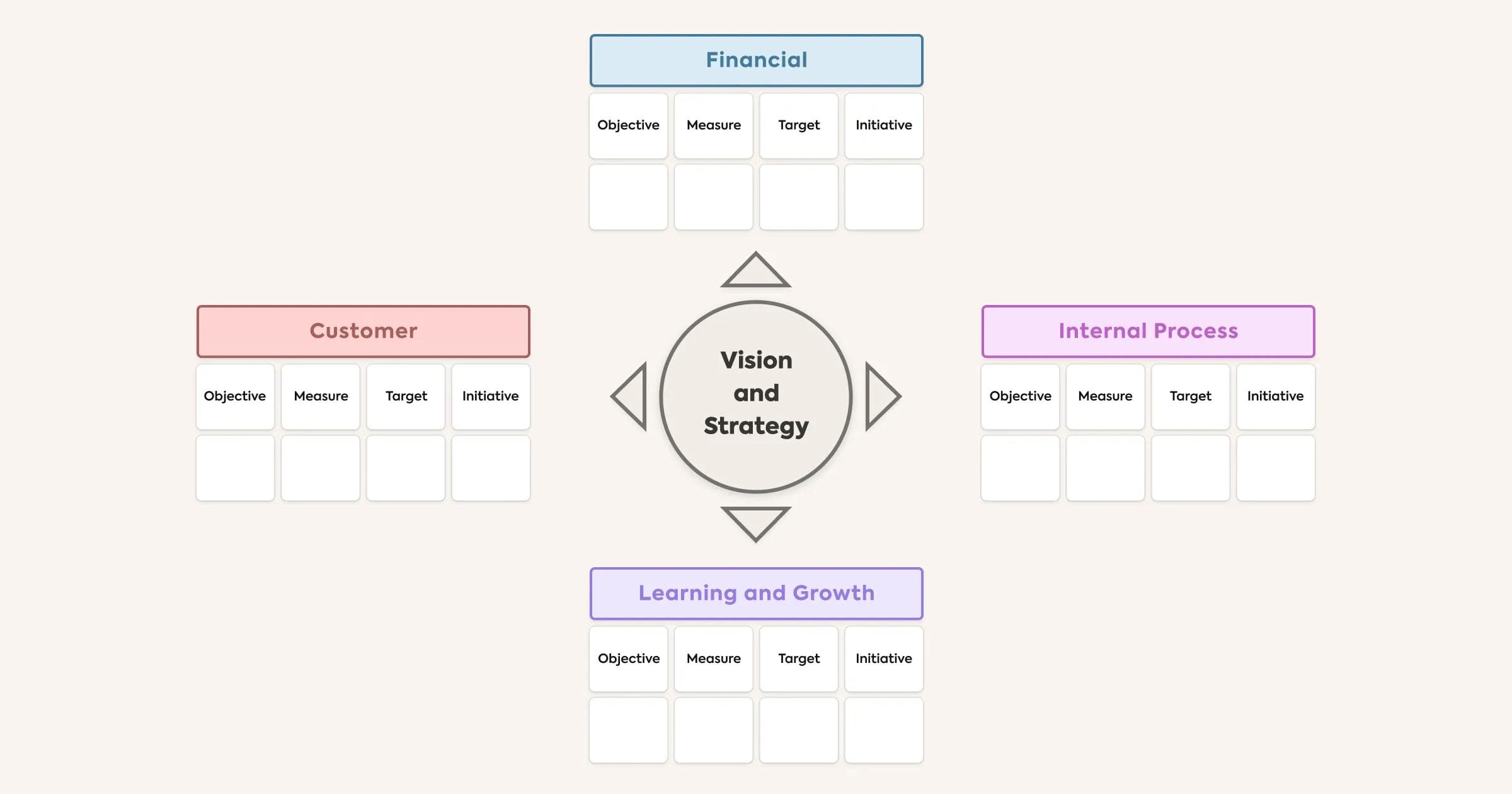

The four perspectives of the Balanced Scorecard

According to its name, the Balanced Scorecard should be balanced. The performance of a company is therefore always viewed from four perspectives:

- The financial perspective includes traditional financial measures, e.g. profit, sales, and return on investment. The focus is on the profitability of the company and the interests of the shareholders.

- The customer perspective shows whether the wishes of the customers are being fulfilled. Examples of key figures here are customer satisfaction, customer complaints, the repurchase rate or recommendations.

- The internal business processes perspective describes how smoothly (or poorly) internal business processes run. For example, lead times, the rework rate or the error rate can be used as key figures for measuring internal business process performance.

- The learning and growth perspective shows how well the company is geared to the future and can grow and exploit potential. Among other things, product innovations, employee satisfaction or the company's image are measured here.

Origin of the Balanced Scorecard

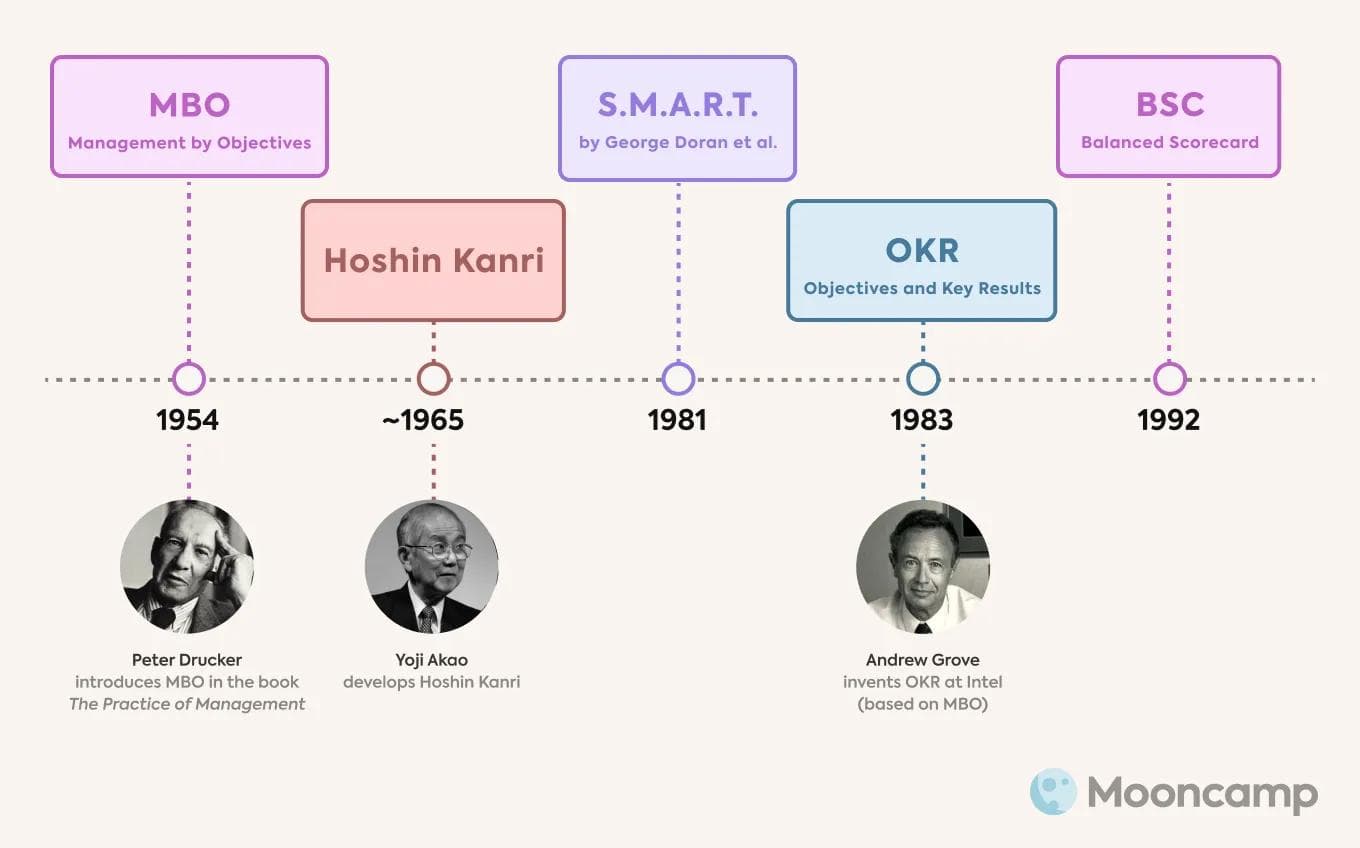

The Balanced Scorecard concept can be traced back to a study conducted in the early 1990s under the direction of Robert S. Kaplan and David P. Norton that was first published in the Harvard Business Review. In it, the U.S. researchers examined various performance measurement models. The aim was to find a model that goes beyond pure financial performance and also takes non-financial indicators into account – thus painting a balanced, holistic and realistic picture of a company.

In order to achieve this goal, Kaplan and Norton developed the Balanced Scorecard system, which, in addition to the financial success, also includes the customer, process and growth perspectives and thus makes it possible to set up a balanced system of goals and key performance indicators.

BSC in strategic management – how it works

A Balanced Scorecard can be developed and implemented in six steps, which we have summarized here. The focus is always on the individual strategy of a company.

1. Formulate vision and strategy

The basis for a Balanced Scorecard is always a clear and long-term vision or corporate strategy. In order to create a Balanced Scorecard, entrepreneurs should therefore first and foremost address the following questions:

- What is our philosophy?

- What market position are we aiming for? What do we want to achieve?

- What is our strategy?

- What differentiates us from the competition?

2. Define strategic objectives, key figures and targets

The second step is to define the metrics, strategic objectives and success factors (or targets) that need to be achieved in order to accomplish the overarching vision. These are defined from the viewpoint of the four Balanced Scorecard perspectives using the following questions:

- What strategic objectives are to be achieved?

- What performance measures do we use to evaluate these goals?

- What are the specific targets? Where do we want to get to?

The goal is to achieve a strategy that is as balanced as possible and that focuses equally on all areas of organizational performance. In practice, several objectives are usually selected for each perspective. However, to ensure the clarity of the key performance indicator systems, there should be no more than five KPIs per perspective.

3. Define actions to achieve the strategic goals

The scorecard must also include concrete actions. Once objectives, targets and measures have been set, entrepreneurs should ask themselves about the activities needed to achieve these goals. The answer to this question is recorded in the Balanced Scorecard for each individual goal.

4. Visualize the Balanced Scorecard

A Balanced Scorecard is only useful if it is presented in such a way that the goals, targets and indicators are understood by everyone in the company. Only in this form can the scorecard be successfully communicated and embedded in daily work. Finally, employees must know which actions they should implement in order to achieve the strategic objectives.

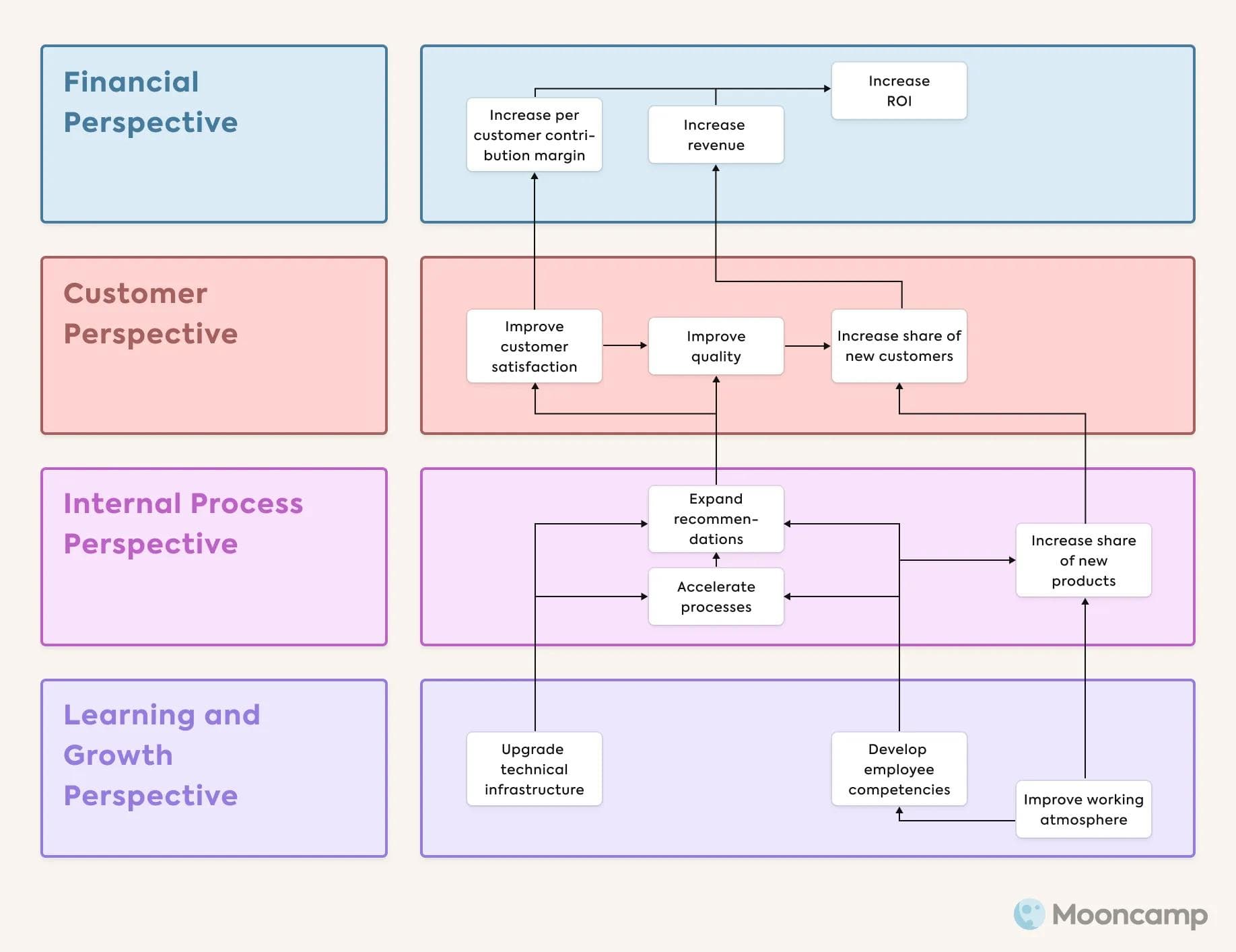

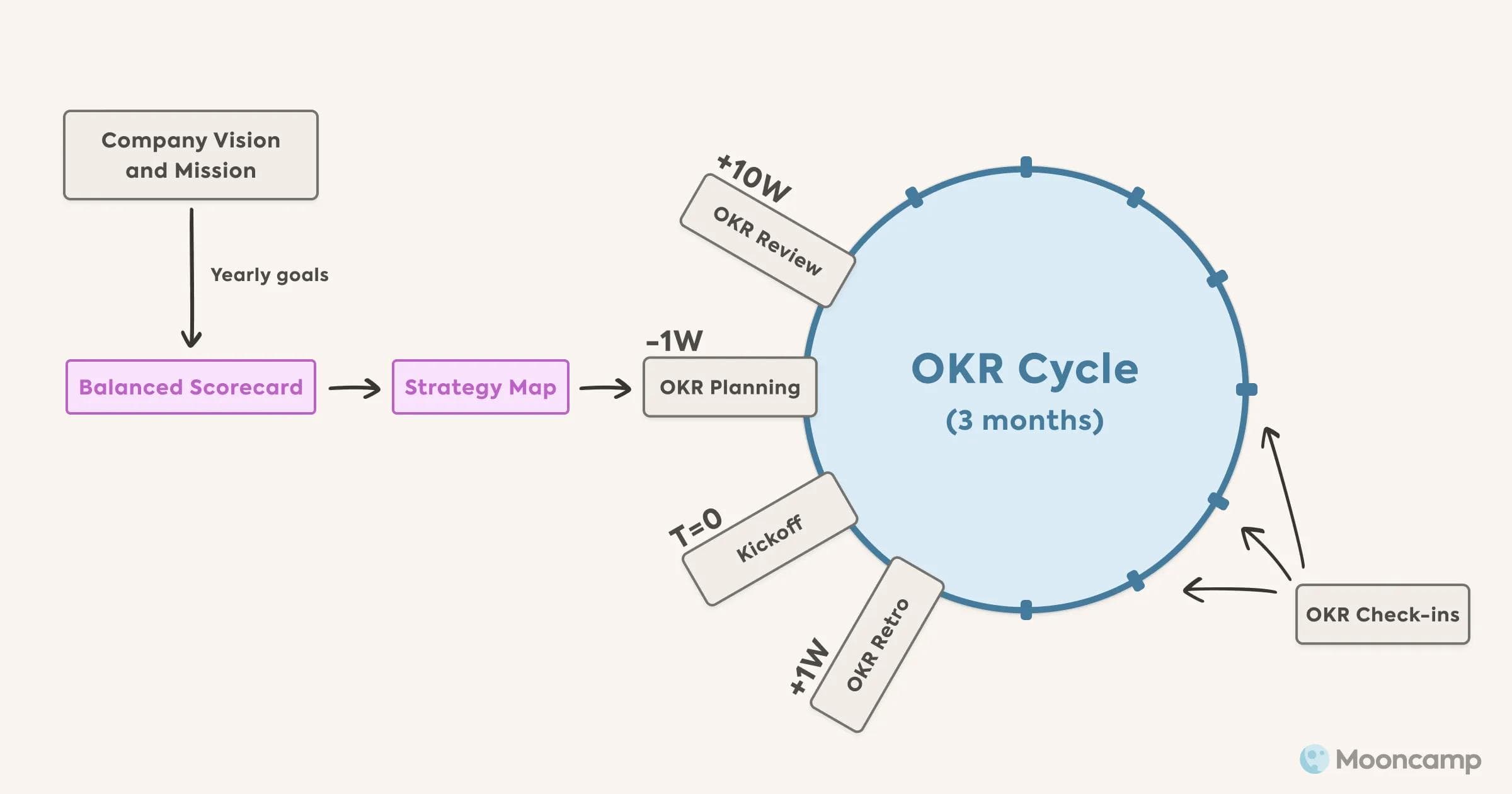

5. Use strategy mapping for implementation

The most impressive strategy is of no use if it only exists on paper and in the minds of management. Translating strategy in such a way that all employees are aware of it and know what it means for their daily actions at work is crucial. This is precisely why Kaplan and Norton developed the strategy map together with the balanced scorecard approach. In it, the strategic initiatives from the BSC are distributed across all four perspectives as if on a map, so that it becomes clear how everything is interrelated.

This means that traditional financial performance measures such as profit or sales are linked to customer satisfaction, for example, and it is shown how training programs for employees can optimize internal processes and thus improve quality or increase sales.

Steps four and five go hand in hand: Both serve to highlight and make visible what is really important – and to ensure that all employees can also (visually) understand this.

6. Continuously develop the BSC

A balanced scorecard is not something you create once and then rigidly work through. The world of work is constantly changing, requirements vary – and companies should therefore also regularly check their company scorecard and adjust it if necessary. The following questions are helpful:

- Are the goals still valid? Have the goals already been achieved?

- Do all measures still make sense under the current conditions? Which measures may be outdated?

- Are the contents of the BSC still in balance? Are all perspectives still considered equally? At which point should the Balanced Scorecard be adjusted?

What do Balanced Scorecards look like? An example

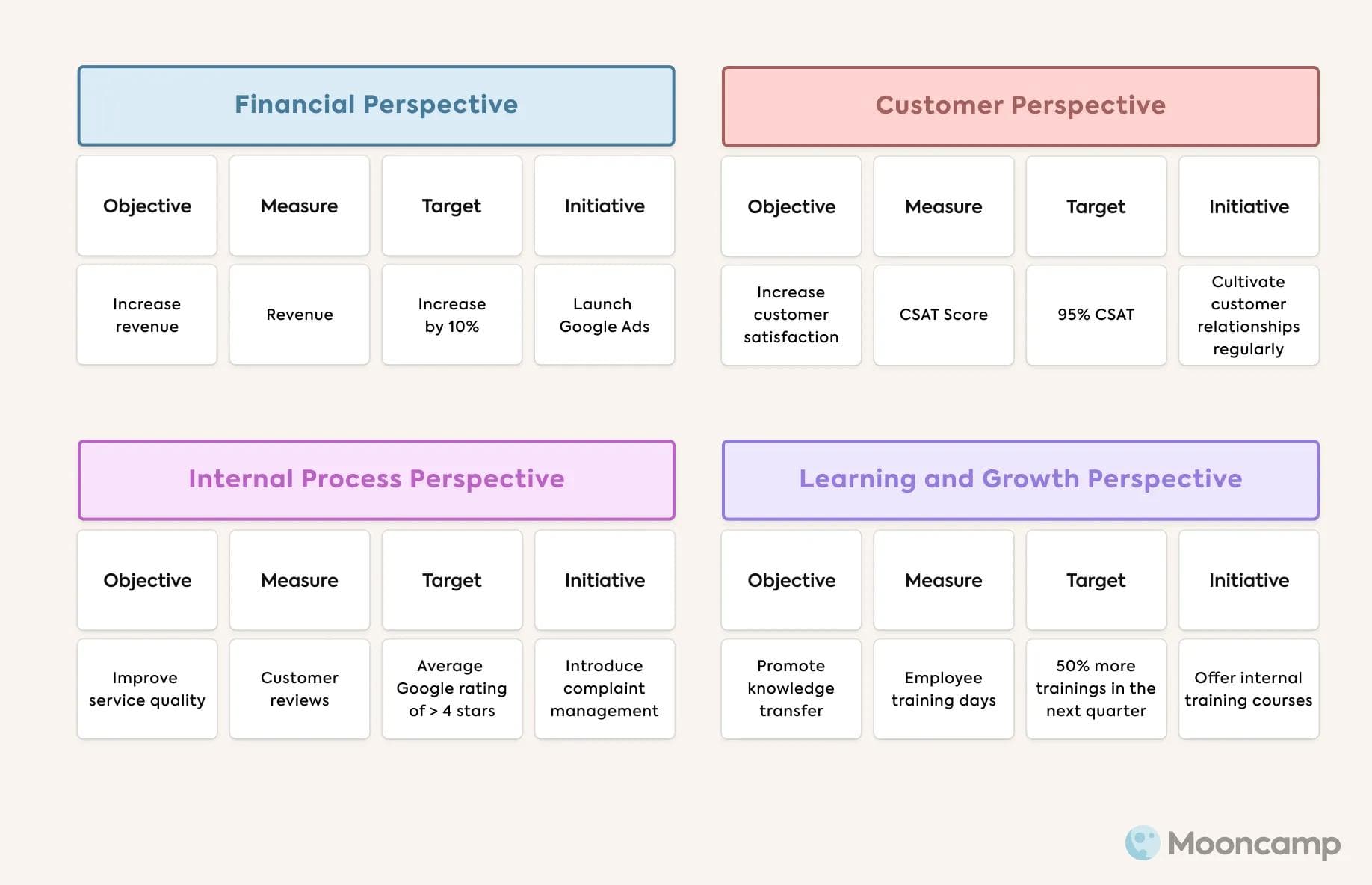

But what does a Balanced Scorecard look like in practice? For a quick overview, we will show you a simplified Balanced Scorecard example with only one strategic objective per perspective. The vision of the company is at the very center.

Financial perspective

- Objective: Increase revenue

- Measure: Revenue

- Target: 10% increase

- Initiative: Place ads on Google; plan and advertise discount promotion via social media

Customer perspective

- Objective: Increase customer satisfaction

- Measure: CSAT Score

- Target: 95% CSAT

- Initiative: Cultivate customer relationships regularly

Process perspective

- Objective: Improve service quality

- Measure: Customer reviews

- Target: Average Google rating of > 4 stars

- Initiative: Introduce complaint management

Learning and growth perspective

- Objective: Promote knowledge transfer

- Measure: Employee training days

- Target: 50% more trainings in the next quarter

- Initiative: Offer internal training courses

How good is the Balanced Scorecard? Pros and cons

While the Balanced Scorecard has proven its worth in the management world over the past 20 years, practical experience also shows that implementation can cause problems. If we take a look at the advantages and disadvantages of the Balanced Scorecard, it quickly becomes clear why this is the case.

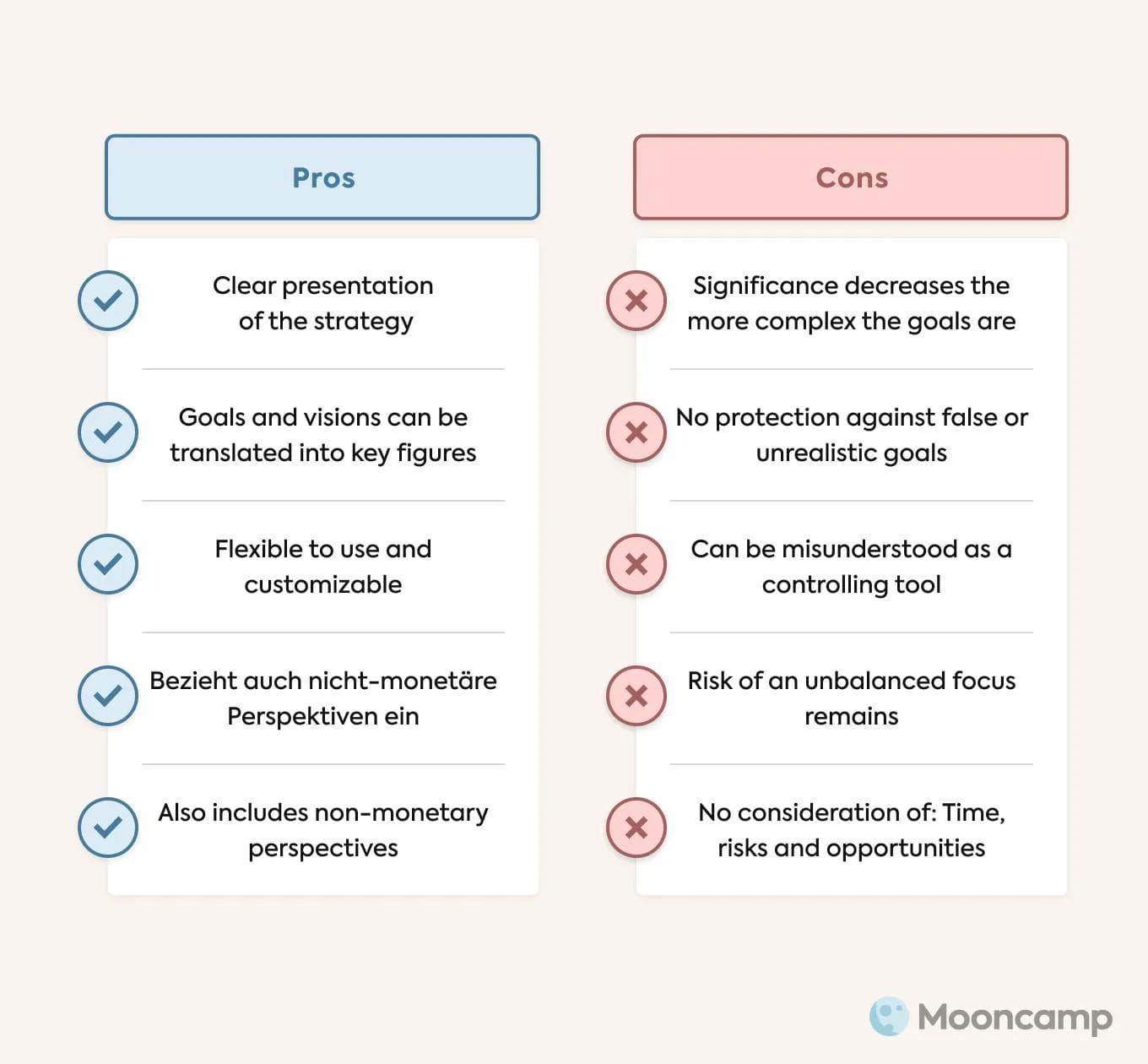

Pros of the Balanced Scorecard

When utilized correctly, the Balanced Scorecard is a powerful management system that can help entrepreneurs maintain an overview of their company's course at all times. Specifically, the Balanced Scorecard has the following advantages:

- It is quite easy to clearly visualize strategies in a balanced scorecard and to present them in a consistent manner.

- Overall goals and visions for a company can be translated into testable key figures with the help of a Balanced Scorecard.

- The Balanced Scorecard is flexible to use and can be customized. Every company that works with it can determine for itself which dimensions and strategic objectives it wants to include.

- In addition to traditional financial accounting measures, the Balanced Scorecard also includes non-monetary perspectives and is therefore not as one-sided as other strategy execution models.

- In the Balanced Scorecard, interdependencies of effects become quickly apparent and are comprehensible to all employees.

Kaplan and Norton themselves express the advantages of the Balanced Scorecard like this:

Cons of the Balanced Scorecard

On the other hand, the Balanced Scorecard also has some major flaws. We have listed these here:

- The informative value of the BSC decreases the more complex the goals on it become and the more numbers and data it contains.

- The concept does not protect against setting wrong or unrealistic goals – because even bad corporate strategies can be mapped on a well-made scorecard.

- The Balanced Scorecard is often misunderstood as a pure controlling tool.

- If companies concentrate too much on individual key figures or areas when creating the BSC, this can lead to the scorecard being less balanced than intended.

- The time dimension as well as risks and opportunities or a competitive analysis are not taken into account in the Balanced Scorecard.

BSC and OKRs – a perfect combination?

If you read articles about strategy and performance management nowadays, you often come across the opinion that the Balanced Scorecard is quite similar to the agile method “Objectives and Key Results (OKR)”. This frequently leads to confusion. Therefore, we would like to shed some light on the subject: The following section shows how OKRs and BSC differ – and why the two frameworks can even be combined well.

One thing is true: OKRs are similar to the BSC in that they also work with strategic objectives and support employees in achieving the jointly defined goals. Ambitious qualitative goals (objectives) are set, each of which is linked to two to four quantitative goals (key results). This makes it easy to monitor whether the company's goals have been achieved. The whole process usually takes place on a quarterly basis.

💡 Tip: If you would like to read up on OKRs in more detail, take a look at our OKR Guide.

This is how OKRs and the Balanced Scorecard differ

As much as the two approaches appear to have in common at first glance, there are many subtle yet important differences:

- OKRs are usually reviewed and redefined on a quarterly basis and thus more regularly than the Balanced Scorecard. The latter is classically set up on an annual basis. This makes OKRs much more flexible when it comes to changes.

- OKRs combine top-down specifications from the management team with bottom-up planning by team members. This makes the process much more transparent and comprehensible for everyone in the company. The Balanced Scorecard, on the other hand, is normally determined exclusively top-down by the executive level.

- OKRs are deliberately set in an inspiring and ambitious way. Achieving one hundred percent of a target is not an absolute necessity – after all, even if an ambitious goal is only partially achieved, one has still accomplished more than by setting lower targets in the first place. BSC, on the other hand, expects all goals to be fully achieved.

- OKRs focus on what is most important for the next quarter, regardless of perspective. A balanced scorecard, on the other hand, always contains the central goals and key performance indicators from four perspectives and follows a fixed structure when it is created.

BSC and OKRs – the best of both worlds

If one sees the two frameworks less as competing methods and more as combinable tools for a strategy focused organization, it becomes clear that they basically mesh perfectly: The Balanced Scorecard helps to choose the right goals and OKRs structure the process of achieving them.

A BSC Strategy Map could be used in addition to OKRs, for example, to clarify the relationships between the objectives for all employees and to illustrate how OKRs can be aligned in a company.

Conversely, a Balanced Scorecard provides a good orientation for meaningful and ambitious Objectives. Executives can use a balanced scorecard to clearly illustrate what is important for the coming year - and then break down the strategy even further per quarter and for individual departments and teams in the form of OKRs.

In other words, a holistic strategy can be developed with the help of the Balanced Scorecard, the implementation of which then happens through OKRs.

As a supplement to the Balanced Scorecard, OKRs ensure that the strategy does not become too macroscopic and contains clear, time-dependent metrics. In addition, OKRs support companies in moving away from purely output-oriented thinking and focusing on relevant results (outcomes).

💡 Tip: On our blog, you'll also find a helpful article on "Output vs. Outcome", where we explain the difference in detail.

💡 By the way, there are other strategic frameworks that can promote a company's success through strategic targets. In addition to Balanced Scorecard and OKR, it is also worth taking a look at MBO, OGSM and Hoshin Kanri.

Conclusion: BSC and OKRs are stronger together

In summary, the Balanced Scorecard is an attempt to provide companies with a tool for the strategic planning process by means of goal setting that can cope with the complexity of today's working world and even actively incorporate it. Experience has shown that traditional performance measurement systems are no longer suitable for the strategic management of companies, or only to a limited extent.

While the BSC alone has proven itself, but also has to contend with some weaknesses, a mix of methods – for example with OKRs – could be an even better way for a company to set itself up for strategic success and agility.

After all, working with one management method does not mean that other methods must automatically be excluded.

Balanced Scorecard – FAQ

What is the Balanced Scorecard?

The Balanced Scorecard links particularly important strategic objectives of a company with key performance indicators and thereby translates the vision and mission of a company into measurable key figures. It thus provides a constant overview of the company's course.

How do you make a Balanced Scorecard?

A Balanced Scorecard can be created in six steps: 1️⃣ Formulate vision and strategy. 2️⃣ Define objectives, metrics and targets. 3️⃣ Determine actions to achieve strategic goals. 4️⃣ Visualize Balanced Scorecard. 5️⃣ Develop strategy map for implementation. 6️⃣ Continuously develop BSC.

Why do you need a balanced scorecard?

Classical measurement systems for strategic performance usually focus exclusively on financial aspects and are very complicated and differentiated. The BSC, on the other hand, offers the simplest possible method for measuring performance, which also includes non-monetary aspects and breaks down an overarching strategy to to what is most important to all employees.

Which metrics can be used for BSC?

Metrics can vary by industry or company. Common metrics for the financial perspective are: sales, return on investment, revenue. From the customer perspective, one could use product quality, new customer share and order behavior. Lead time, complaint rate and error rate can be assigned to the process perspective. And from the development perspective, metrics like training days, employee satisfaction and staff turnover are possible.